China Declares Stablecoins Illegal, Intensifies Crypto Crackdown

China declared stablecoins illegal in the latest escalation of its sweeping crackdown on cryptocurrencies.

According to a Nov. 30 report by the official China Daily newspaper, the declaration was made after a meeting of 13 government agencies, including the Ministry of Public Security and the Office of the Central Cyberspace Affairs Commission.

The agencies highlighted the recent resurgence in speculative trading, which they warned bring new risks and challenges for regulators.

The central bank made its clearest statement yet ”that stablecoins fall within the scope of illegal financial activities, bringing them further under the onshore monitoring and enforcement framework,” the newspaper said.

Virtual Assets Don’t Have Same Legal Status As Fiat

One of the main statements made by the PBOC on the day was that virtual currencies do not have the same legal status as fiat money, with the central bank saying that these assets “must not be used in the market as currency.” The central bank also said that all related activities are deemed illegal.

Commenting on the rapid growth seen in the stablecoin market, the PBOC said that these tokens currently fail to meet the requirements for customer identification and anti-money laundering (AML) safeguards.

As such, it warned that stablecoins, which are pegged to stable assets, could be used for fraud, money laundering, or illicit cross-border fund transfers.

The authorities pledged to maintain their focus on risk prevention while upholding China’s ban on digital currencies.

They also said that they would “deepen coordination and cooperation” in tracking down crypto users by strengthening information sharing and enhancing their monitoring capabilities.

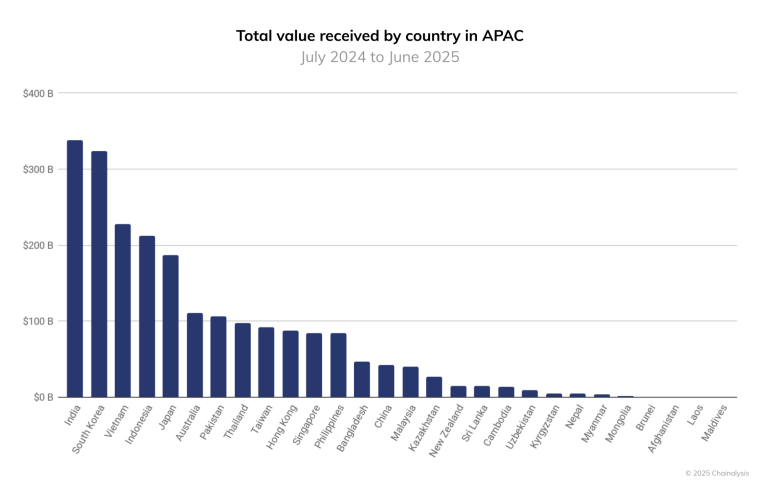

The agencies’ latest reiteration of their anti-crypto stance comes after Chainalysis reported that on-chain value across Asia-Pacific jumped 69% to $2.36 trillion during the year ending June 2025 from a year earlier.

Total crypto value received by country in APAC (Source: Chainalysis)

China Has Cracked Down On Crypto Since 2013

China’s crackdown on crypto started back in 2013, when the PBOC and other authorities issued a notice banning financial institutions and payment processors from providing Bitcoin-related services. These included custodial services, exchanges, and payment or settlement services.

A year later, commercial banks and payment companies were ordered to close accounts used for crypto trading, restricting access on fiat-to-crypto rails.

In 2017, amid the initial coin offering (ICO) boom, Chinese authorities declared that these token raises constituted illegal public financing and banned them. Domestic crypto exchanges were also told to shut down or move offshore.

In 2021, it carried out another sweeping ban, expanding on earlier crackdowns to prohibit financial institutions, payment processors, and others from offering any services related to crypto transactions.

Other Asian Regions Adopt Crypto

While Mainland China cracks down crypto, other parts of the region are adopting digital assets. Among them are Hong Kong and Singapore, which are striving to become regional crypto hubs.

Meanwhile, Japan’s regulatory authority proposed sweeping changes earlier this year that include reclassifying crypto assets as financial products.