Stablecoins Could Pull $1 Trillion From Emerging Market Banks—Standard Chartered

Standard Chartered has estimated that by 2028, more than $1 trillion could move from emerging market banks into stablecoins as the adoption of digital assets increases. The stable nature of these digital assets has made them very attractive in countries with currency crises, like Argentina.

As stablecoin adoption accelerates in developing countries, Standard Chartered projects that its use in these regions could account for 61% of the stablecoin market cap by 2028.

More Than $1 Trillion Could Flow Into Stablecoins in Emerging Markets

In a Monday investor’s note, Standard Chartered’s Global Research department predicted that $1 trillion worth of deposits could flow out of emerging economy banks into stablecoins over the next three years.

The report notes that approximately two-thirds of the current global stablecoin supply is held in emerging markets. The report explained that stablecoins have become very attractive to emerging markets (EMs) because 99% of all these assets are pegged to the dollar.

With stablecoins providing dollar-based bank accounts to individuals in parts of the world prone to currency crises, they have turned to these assets even more. The desire to avoid their savings being wiped out has forced individuals and companies to put their money into stablecoin wallets instead of banks.

Because of this, Standard Chartered estimates that the stablecoin in EMs could rise from $173 billion today to $1.22 trillion within three years. The bank estimated that the global market cap of stablecoins could rise from $310 billion today to over $2 trillion by 2028.

What’s Fueling the Stablecoin Drive in Emerging Markets

Standard Chartered opined that the most significant disruption to the stablecoin market will come from emerging markets, where access to the US dollar was historically restricted.

Stablecoins offer lower credit risks to the deposits in their local banks by offering their consumers digital, 24/7 access to a USD account, as, according to the GENIUS Act in the United States, they must be backed by dollars entirely.

Standard Chartered claimed that this dynamic increases the threat of deposits into traditional banks in EMs. Another major factor that could ignite the move of funds from traditional banks into stablecoins is the high inflation in countries with low reserves and high remittance inflows.

Stablecoins reduce the cost of remittances, as well as speed up remittances to people who receive money abroad. In the case of unstable local banks or pressure on them by the government, stablecoins are viewed as more trustworthy. This transition is already occurring in places such as Venezuela, with annual inflation between 200% and 300%.

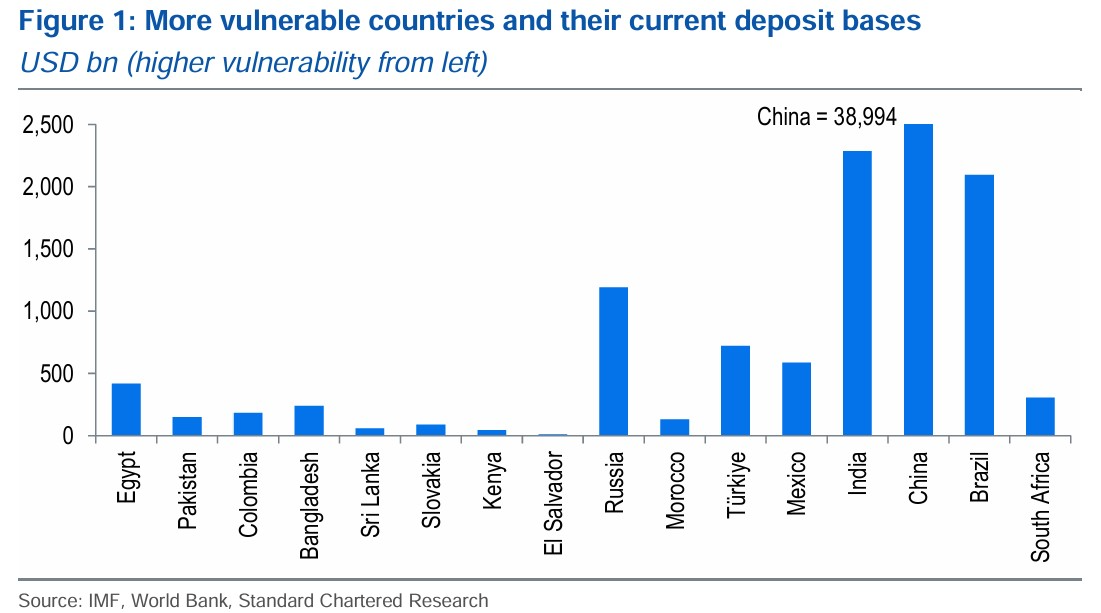

Inflation is no longer under control, and now many Venezuelans use USDT (Tether) to make daily payments. Stores even display the price in stablecoins rather than in the local currency. The report highlighted Bangladesh, Colombia, Egypt, Pakistan, and Sri Lanka as the most vulnerable countries to capital flight from banks to stablecoins.

With other EMs facing inflation turning to stablecoins as a safe haven, Standard Chartered anticipates that this will fuel the massive growth in these regions.

What This Means for Banks in Emerging Markets

Over the next few years, people in emerging markets could completely change how they store and move their money. The increasing adoption of stablecoins could cause banks to lose big deposits, thus increasing their funding costs and reducing their lending ability. To keep up with the global adoption of stablecoins, these banks might need to change their business models.