Wall Street Banks From JPMorgan To Bank Of America ‘Debanked’ Customers Improperly, Regulator Says

Nine of the US’s largest banks, including JPMorgan and Citibank, ”debanked” customers improperly, The Office of the Comptroller of the Currency (OCC) said.

A Dec. 10 OCC press release said the nine banks had made ”inappropriate distinctions in the provision of financial services” to companies in industries including oil and gas exploration, coal mining, firearms, private prisons, tobacco and e-cigarette manufacturers, adult entertainment, and digital assets.

“It is unfortunate that the nation’s largest banks thought these harmful debanking policies were an appropriate use of their government-granted charter and market power,” Comptroller of the Currency Jonathan Gould said.

The OCC identified instances where at least one bank imposed restrictions on certain industry sectors because they engaged in “activities that, while not illegal, are contrary to [the bank’s] values.”

“While many of these policies were undertaken in plain sight and even announced publicly, certain banks have continued to insist that they did not engage in debanking,” Gould said. “Going forward, the OCC will hold banks accountable for these actions and ensure unlawful debanking does not continue.”

The other seven banks named were Chase Bank, Wells Fargo, US Bank, Capital One, PNC Bank, TD Bank, and BMO Bank.

”The OCC’s findings confirm that these or similar policies and practices were in place at each of the banks reviewed,” the regulator said.

The report follows President Donald Trump’s signing of an executive order to investigate suspected debanking practices.

Operation Chokepoint 2.0

Banks’ hostility toward the crypto industry became known as Operation Choke Point 2.0, under which government agencies and banks were perceived to be informally discriminating against what they saw as a high-risk industry.

Trump and his family have also claimed they were debanked for political reasons while Trump was out of office. Multiple senior crypto industry figures have said their bank accounts were closed without explanation or that they were denied banking services.

The situation has improved since Trump entered the White House, but there are still some reports that debanking issues persist.

In November, the CEO of the Bitcoin Lightning Network payment company Strike, Jack Mallers, said that JPMorgan had abruptly closed his account.

Banks Say They Are Following The Law

Banks have maintained that their decisions to close bank accounts related to certain clients are because they follow laws that require financial institutions to watch for criminal activity and money laundering.

The Bank Policy Institute, a lobbying group for banks, said yesterday that the industry supports creating new rules to ensure fair access to banking.

“It’s in banks’ best interest to take deposits, lend to, and support as many consumers and businesses as possible to drive economic growth,” the group said.

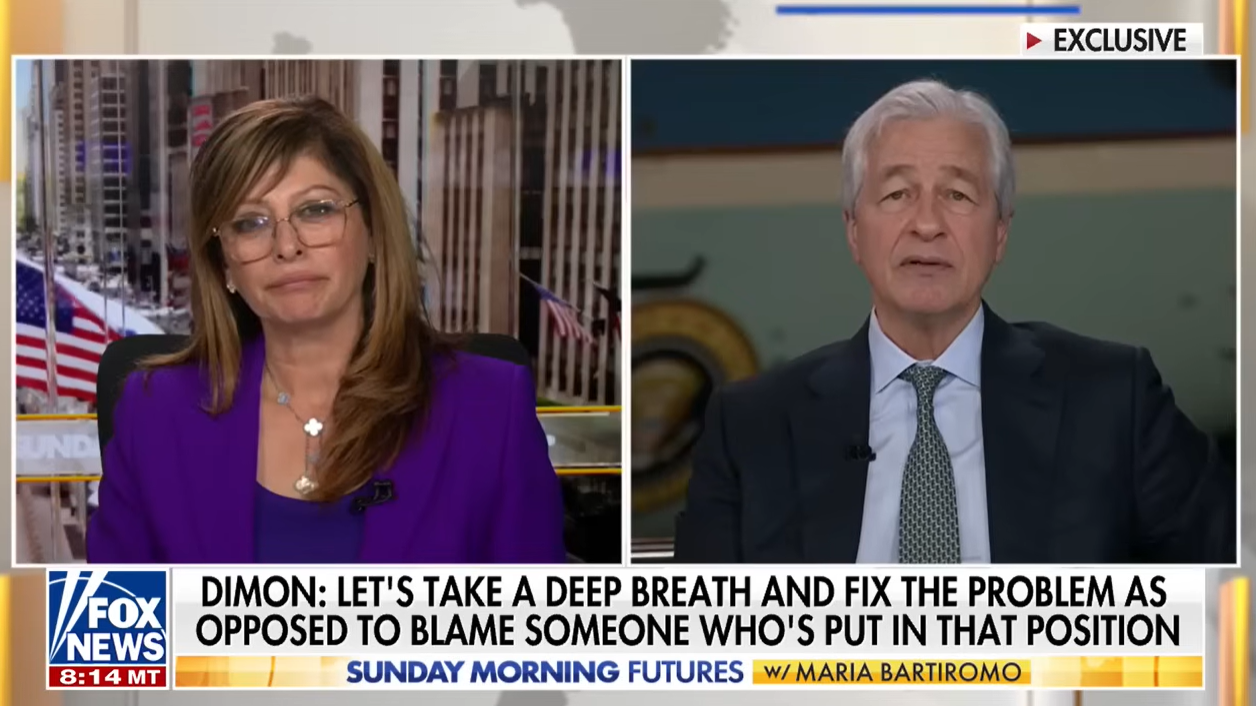

On Sunday, JPMorgan CEO Jamie Dimon denied that his bank closes accounts belonging to customers based on their religious or political affiliation.

“People have to grow up here, OK, and stop making up things and stuff like that,” Dimon said during an interview with Fox News. “We do not debank people for religious or political affiliations.”

Jamie Dimon maintains JPMorgan doesn’t debank people for political affiliations (Source: YouTube)

Dimon applauded the Trump administration for addressing debanking, and said that he has been asking for the rules to change for 15 years.

“It is really customer unfriendly, and we’re debanking people because of suspected things, or negative media, or all these various things,” Dimon said.